GLOBAL THREAT ANALYSIS | INTELLIGENCEANALYSIS.ORG

WEEKLY BRIEF | 14 JUNE - 20 JUNE 2026

THE WORLD AFTER THE DEAL: IRAN, HORMUZ, AND THE ARCHITECTURE OF A FRAGILE PEACE

EXECUTIVE SUMMARY

Welcome to this week’s Global Threat Analysis from INTELLIGENCEANALYSIS.ORG. The week of 14 to 20 June 2026 will be marked in the historical record as the moment the world’s most consequential energy chokepoint began its slow return to functionality, as the United States and Iran signed a 14-point memorandum of understanding at the Palace of Versailles on 17 June, formally committing both nations to an end of hostilities and the staged reopening of the Strait of Hormuz. But peace on paper and peace in practice are very different things. The MOU is provisional, leaves the most contentious issues unresolved, and gives both sides 60 days to reach a final agreement -- a timeline most analysts regard as optimistic at best. Meanwhile the G7 summit in Evian-les-Bains closed with real but limited outcomes on trade and Ukraine support, Ukraine’s frontlines remained locked in attritional stalemate as peace talks stalled on territory, China quietly escalated pressure on Taiwan’s South China Sea outposts, the Sahel continued its slide toward systemic collapse, and cybercriminals and state-linked hackers exploited a world distracted by war. What follows is a complete analytical survey of the week’s most significant developments across every major region and threat domain.

TOP DEVELOPMENTS THIS WEEK

1. THE US-IRAN MEMORANDUM OF UNDERSTANDING

The most significant geopolitical event of the week -- and arguably of the year so far -- was the signing of a 14-point memorandum of understanding between the United States and Iran.

President Donald Trump signed the document on the evening of 17 June at the Palace of Versailles, with French President Emmanuel Macron present. Iranian President Masoud Pezeshkian signed separately, and Iran’s Foreign Ministry confirmed the agreement had entered into effect.

The MOU commits both sides to an immediate and permanent termination of military operations on all fronts, including in Lebanon. Iran agreed to use its best efforts to allow safe passage for commercial vessels through the Strait of Hormuz within 60 days of signing, with mine clearance to begin immediately. The US agreed to lift its naval blockade of Iranian ports. Sanctions waivers were included, and Iran will be permitted to sell oil freely during the negotiation period. A 60-day window, extendable by mutual consent, was set for talks on a final agreement covering Iran’s nuclear programme, ballistic missile programme, and the scope of permanent sanctions relief.

Qatar and Pakistan served as co-mediators. Pakistani Prime Minister Shehbaz Sharif announced the deal minutes before Trump confirmed it on social media. Trump lifted the US naval blockade by executive statement, writing: “Ships of the world, start your engines.”

What the MOU does not resolve is everything that made this war possible. Iran’s nuclear programme is addressed only in terms of future talks, not binding commitments. The IAEA has been unable to resume inspections inside Iran since the June 2025 strikes on Iranian nuclear sites. Whether Iran still possesses sufficient enriched uranium to pursue a weapon within weeks of choosing to do so remains unknown. The agreement also raises the prospect of a renegotiation of US military presence in the region, a point that alarmed Israel’s government. Prime Minister Netanyahu sought a meeting with Trump in the days immediately following the signing.

The MOU is, at this stage, a framework for stopping the bleeding. It is not a peace settlement.

2. G7 EVIAN SUMMIT: LIMITED CONSENSUS, VISIBLE FRACTURES

The 52nd G7 summit was held in Evian-les-Bains, France, from 15 to 17 June 2026, hosted by President Macron.

The summit agenda was dominated by four converging crises: the Strait of Hormuz closure and its energy market effects, a looming expiry of Trump’s Section 122 tariff authority on 24 July, a critical minerals emergency driven by Chinese export restrictions, and the ongoing demand for Western support to Ukraine.

On energy and Iran, the summit’s timing proved fortunate. The MOU signing occurred on the final day, and G7 leaders issued a joint statement welcoming the deal and calling for swift implementation.

On trade, the outcomes were more modest. Leaders agreed to coordinate on Chinese industrial overcapacity across EVs, solar components, wind turbines, and semiconductors. France and Germany announced a joint definition of “sovereign technology” tied to measurable criteria including company headquarters, data location, R&D presence, and workforce. The summit also acknowledged the approaching July 24 tariff cliff, where Trump’s Section 122 authority expires without congressional extension. Congress has not passed extension legislation, and no extension bill has cleared committee. If the authority lapses, the 15 percent universal import tariff on most US trading partners falls away automatically unless replaced by other legal instruments.

On Ukraine, G7 members agreed to increase military support, including additional air defence systems and interceptors.

The summit revealed a transatlantic trust deficit that the Iran deal did not fully repair. A survey published by the European Council on Foreign Relations found that only 11 percent of Europeans now view the United States as an ally, down from 16 percent six months ago. Canadian Prime Minister Mark Carney delivered a pointed address at Trinity College Dublin on the eve of the summit, characterising current conditions as a “global rupture, not a quiet transition.”

3. UKRAINE: STALEMATE, TALKS, AND EUROPEAN ALARM

The Russia-Ukraine war entered its fifth year with no decisive military shift and no credible peace framework in place.

Frontline data from the Institute for the Study of War showed Russia recording a net loss of approximately 93 square miles of Ukrainian territory during the four-week period ending 3 June. Ukraine’s own OSINT tracking group DeepState, however, recorded a smaller Russian net gain of 3 square miles over the same period. The discrepancy reflects the difference between ISW’s analysis methodology and real-time ground reporting, and the truth likely lies somewhere between these figures. The takeaway is that the front is grinding, not moving.

On diplomacy, a joint statement was issued on 7 June by the UK, France, and Germany alongside President Zelenskyy, supporting direct Russia-Ukraine dialogue while insisting all ceasefire efforts must be coordinated with Europe and the United States. The Kremlin responded two days later by dismissing the joint statement as words without substance, arguing that Western nations were simultaneously planning new weapons deliveries to Kyiv.

Russian Foreign Ministry spokesperson Maria Zakharova stated on 11 June that the conditions contained in the European mediation framework were completely unacceptable to Moscow.

The fundamental disagreement remains unchanged. Russia demands international recognition of its annexation of Crimea, Luhansk, Donetsk, Zaporizhzhia, and Kherson. Ukraine and its European partners regard these demands as non-starters. The US deadline for a peace agreement by June appears to have passed without a breakthrough.

Public polling within both countries shows movement. Surveys indicate that 62 percent of Russians support peace negotiations, while 61 percent of Ukrainians now support some form of territorial compromise to end the war. These figures do not reflect a political consensus -- they reflect war fatigue on both sides, which is not the same thing.

REGIONAL ANALYSIS

MIDDLE EAST

The signing of the US-Iran MOU was the dominant event of the week for the region, but the surrounding picture is more complicated than the headlines suggest.

The Strait of Hormuz has been effectively closed since late February 2026, when the IRGC imposed a maritime blockade in response to US and Israeli strikes on Iran. Middle Eastern oil producers have cut output by more than 11 million barrels per day. Global oil inventories in OECD countries fell to their lowest levels since 2003. Brent crude averaged around $105 per barrel in June, down from a high above $140 reached at the peak of hostilities, but still well above pre-conflict levels of roughly $70.

The MOU commits Iran to begin mine clearance within 30 days and to allow commercial traffic to resume progressively. Iran’s position on long-term management of the strait -- including charging service fees -- puts it in tension with Trump’s stated commitment to a permanently toll-free passage. This discrepancy will likely be a pressure point during the 60-day negotiating window.

Israel is the most significant wildcard. Israel was a belligerent in the original conflict. The MOU’s reference to ending hostilities “including in Lebanon” suggests the deal is intended to include Hezbollah and the Israel-Lebanon front, but Israeli officials have not formally signed on to the framework. Netanyahu’s effort to secure a direct meeting with Trump in the days following the signing suggests significant Israeli dissatisfaction with the terms, particularly regarding Iran’s nuclear programme and the fate of enriched uranium stockpiles.

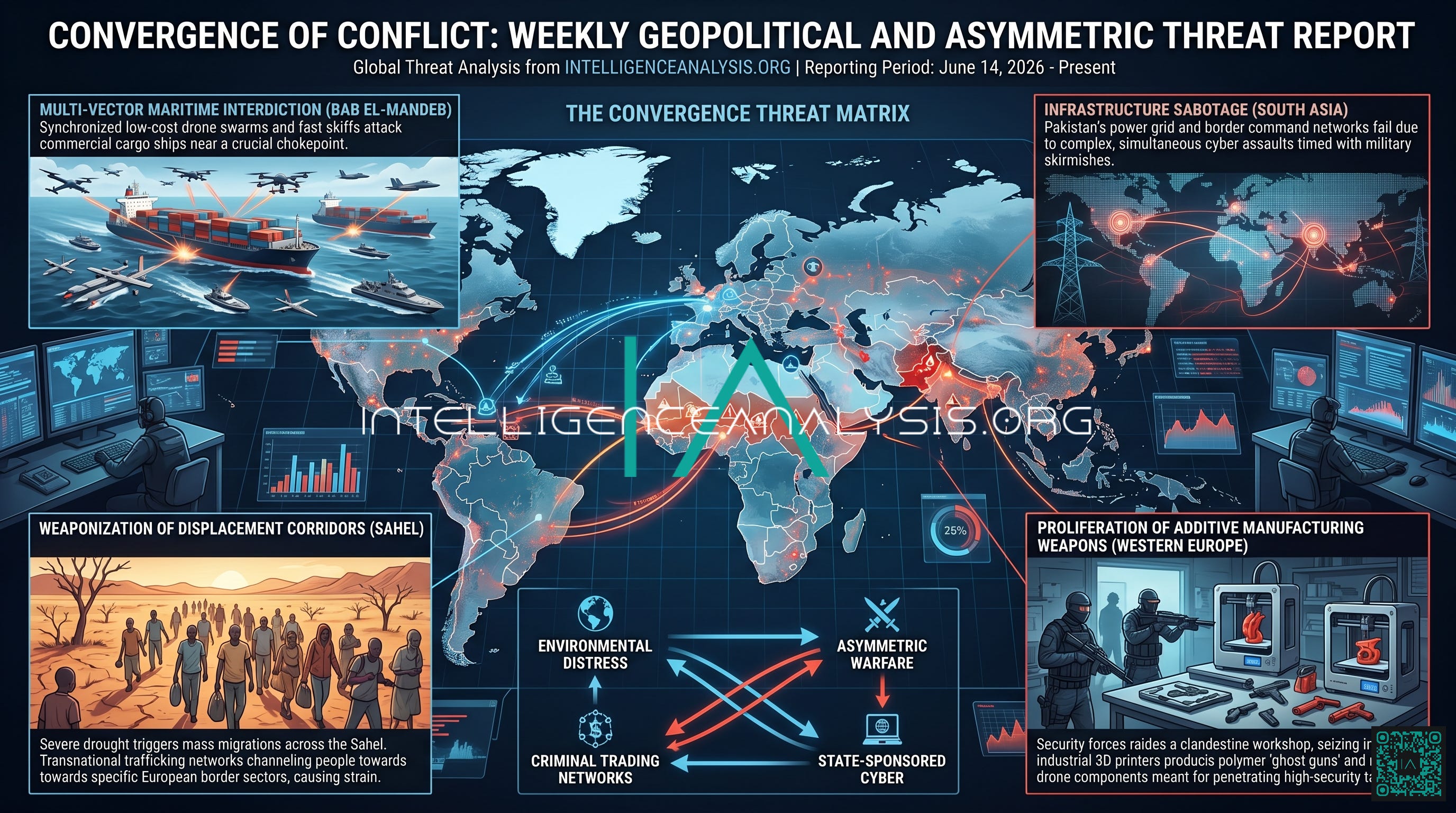

Hezbollah’s continued use of fiber-optic-guided FPV drones, which are immune to electronic jamming, has caused significant casualties among Israeli forces and created deep concern within the Israeli defence establishment. Reports from May and June indicate these attacks have persisted through the ceasefire period. Israel’s “unlimited budget” commitment to countering this threat signals that the drone war in Lebanon is not over simply because a deal has been signed.

Yemen and the Houthi question also remain unresolved. Although major Houthi attacks on commercial shipping paused following the Israel-Gaza ceasefire of October 2025, the movement retains capability and has demonstrated willingness to resume operations in response to regional events. The US Maritime Advisory for the Red Sea and Gulf of Aden remains in effect, warning commercial operators that the Houthi threat persists even without active attacks.

Gaza was not addressed substantively in the MOU. The humanitarian situation in Gaza remains catastrophic. The deal’s reference to ending hostilities “in Lebanon” does not create a formal mechanism for Gaza reconstruction or governance transition.

Iran’s new Supreme Leader, Mojtaba Khamenei, son of the assassinated Ali Khamenei, accepted the MOU. His consolidation of power within Iran’s fractured political system remains uncertain, and his ultimate position on nuclear negotiations cannot yet be assessed with confidence.

EAST ASIA

China continued its campaign of grey-zone pressure against Taiwan and the Philippines during the week, with notable escalations in the South China Sea.

Taiwan’s Coast Guard reported, on 14 June, that mainland Chinese law enforcement vessels had appeared near Taiwan-controlled Pratas Island (Dongsha) in the South China Sea -- the first such confirmed instance involving coordinated CCG and PRC research vessels patrolling Taiwan’s restricted waters simultaneously. CCG vessel 3501 circled Pratas twice over a 24-hour period beginning 5 June, while a PRC research vessel, the Hai Si Lu 6, sailed along the island’s restricted waters perimeter -- a first recorded instance of such coordination.

Beijing sanctioned Philippine Defence Secretary Gilberto Teodoro in the week, marking the first time China has sanctioned a sitting defence official of a nation it formally recognises. The move is a significant escalation of coercive diplomacy and signals Beijing’s growing frustration with Manila’s resistance to Chinese maritime claims in the South China Sea. The PRC has framed the deterioration of relations as the fault of “anti-China” officials rather than government policy -- a framing designed to create political space for future engagement while maintaining pressure.

Taiwan’s Aerospace Industrial Development Corporation announced on 1 June the development of a drone navigation system not reliant on GPS signals -- a direct response to the demonstrated vulnerability of GPS-dependent systems in modern conflict environments, including in Ukraine.

The broader context is the Trump-Xi summit of 13-15 May, which left Taiwan’s government deeply uncertain about the degree of US commitment to its defence. Beijing has moved quickly to exploit that uncertainty.

Japanese-Philippine defence cooperation continued to deepen, with technology transfer agreements aimed at expanding the Philippine Navy’s surface fleet capabilities. The PRC’s Ministry of Transport conducted a “special maritime law enforcement operation” east of Taiwan specifically to contest Japanese-Philippine EEZ delimitation talks in that area.

The South China Sea Code of Conduct negotiations, with a Philippine-backed deadline of end-2026, remain stalled. ASEAN’s ability to reach a meaningful Code of Conduct has been structurally limited by China’s consistent preference for bilateral rather than multilateral frameworks.

EUROPE AND THE UKRAINE WAR

European governments entered the week with Ukraine at the top of their security agendas, but the Iran deal dominated the diplomatic bandwidth of the G7 summit.

The UK, France, and Germany’s joint statement of 7 June, supporting direct Russia-Ukraine dialogue while insisting on coordinated frameworks with allies, was a deliberate signal that Europe intends to remain relevant to any eventual settlement. The Kremlin’s dismissal of the statement as contradictory -- noting that Europe speaks of peace while planning weapons transfers -- reflects the fundamental stalemate in the diplomatic environment.

European defence spending continued to rise, though the pace varies significantly across NATO members. The shift from a position of nominal compliance with NATO’s 2 percent GDP target to genuine rearmament is now visible in several economies, particularly Poland, the Baltic states, and the Nordic countries.

The energy dimension of the Ukraine war also remained live. Europe’s share of LNG imports from Qatar fell to 6 percent in the first quarter of 2026, due to the Hormuz closure limiting Qatari exports. US LNG, the most expensive option for European buyers, has become a structural necessity rather than a market choice. The MOU’s commitment to reopening the strait will eventually ease this pressure, but the IEA and EIA both project that full restoration of pre-conflict production and trade flows will not occur until early 2027 at the earliest.

AFRICA

The Sahel continued its deterioration, with West Africa’s regional security architecture described by the African Security Analysis platform as “entering a decisive phase” on 13 June.

The Alliance of Sahel States -- comprising Mali, Burkina Faso, and Niger -- remains aligned with Russian military support and hostile to both ECOWAS mediation and Western security partnerships. The joint AU-ECOWAS engagement scheduled for Abuja this month was convened at a moment when the institutional response mechanisms are moving demonstrably slower than the threat.

CSIS’s 2026 Global Terrorism Threat Assessment, published earlier in June, identified Africa as the domain of greatest uncertainty in global terrorism, noting that jihadist groups on the continent are “unquestionably ascendant” -- fielding larger forces, commanding greater financial resources, and expanding geographically. African terrorist groups, unlike Middle Eastern counterparts, are growing, not shrinking.

The figures behind these assessments are stark. More than 22,300 fatalities were linked to terrorist groups on the African continent in the 12-month period ending June 2025, a 60 percent increase from 2020-2022. Nearly half of all fatalities occurred in the Sahel. Somalia’s al-Shabaab remains a second major front, with 6,224 fatalities attributed to that group in the year ending June 2025 -- double the figure from 2022.

In the Lake Chad Basin, ISWAP and Boko Haram together account for approximately 18 percent of terror-related deaths on the continent. Although absolute fatalities are lower than their peak, the upward trend continued into 2026.

The convergence of jihadist violence and criminal networks in the Sahel is now well-documented. JNIM has attacked fuel supply lines near Mali’s capital Bamako, targeting economic infrastructure as a deliberate strategy to compound governance failures. In Burkina Faso, the arrest of an influential imam by the military junta in early June exposed the regime’s sensitivity to any independent religious authority that might challenge its legitimacy.

Benin opened engagement with the Sahel juntas in June, a development that may represent an early-stage attempt at regional reset, or may reflect Cotonou’s calculation that neutrality is safer than alignment with ECOWAS’s harder line.

In Central Africa, ADF-ISCAP has expanded operations into Haut-Uele in the DRC, representing a new geographic mutation of the group beyond its traditional strongholds. This expansion intersects with ongoing instability along the DRC-Rwanda-Uganda border.

Ethiopia’s general elections on 1 June 2026 were conducted under elevated political tension and ongoing security pressures in the Tigray, Amhara, and Oromia regions. International observers noted concerns about the environment for political competition.

SOUTH AND CENTRAL ASIA

Pakistan emerged this week as a diplomatic actor of note, serving as co-mediator alongside Qatar in the US-Iran MOU process. Prime Minister Shehbaz Sharif’s announcement of the deal ahead of Trump’s confirmation demonstrates Islamabad’s intent to position itself as a credible neutral broker -- a significant reputational investment for a government managing severe domestic economic pressures.

The implications of a reopened Hormuz are potentially significant for South Asia. India, Pakistan, and Bangladesh all depend heavily on Persian Gulf energy flows and on Gulf remittances from migrant workers. Energy costs in these economies have risen sharply since February 2026.

Afghanistan continues under Taliban governance with no meaningful international recognition. The humanitarian situation remains critical. Cross-border narcotics flows -- primarily heroin from Afghan cultivation -- continue to move through Central Asian and Iranian corridors toward European markets. The disruption of Iran’s economy and governance structure during the war period may have reduced some interdiction capacity along these routes, though data is incomplete.

NORTH AMERICA AND THE CARIBBEAN

The Trump administration’s broader security posture in the Americas remained a significant analytical focus during the week.

The military’s drug boat strike programme in the Caribbean and Pacific continued to generate controversy. A report published on 10 June by The Intercept documented that the first strike of the programme, in September 2025, killed 11 individuals aboard a single vessel -- a number that raised immediate questions at classified briefings about whether those individuals were drug traffickers or human trafficking victims. The US military has conducted more than 60 attacks in nine months, killing over 200 people, with the large crew of the first strike representing a persistent anomaly that has not been officially explained.

This controversy sits at the intersection of the drug trafficking and human trafficking threat domains. The weaponisation of narcotics corridors by cartels to move people is well-documented. When military force is applied to those same corridors without adequate intelligence, the risk of killing trafficking victims rather than perpetrators becomes significant.

On the tariff front, the July 24 cliff date for Section 122 authority remains the most consequential near-term economic policy risk for North America. The tariff structure that has governed US trade relationships with allies for the past year is legally time-limited. Congress has not moved to extend it. The president cannot extend it unilaterally. Whether the administration moves to use alternative legal authorities -- Section 301, national emergency frameworks -- or whether tariffs fall at midnight on 24 July is the central economic policy question for the coming five weeks.

SOUTHEAST ASIA AND THE PACIFIC

ASEAN’s push to finalise a South China Sea Code of Conduct by end-2026 is creating pressure on Indonesia as the pivotal broker state. China’s consistent preference for bilateral frameworks over multilateral agreements means the Code of Conduct negotiations face the same structural constraint they have faced for over a decade.

The Philippines continued to resist Chinese pressure with notable firmness. Defense Secretary Teodoro’s sanctioning by Beijing -- described by analysts as unprecedented -- reflects the PRC’s assessment that Philippine resistance under the Marcos government is more durable than expected, and that targeted personal coercion may succeed where broad bilateral pressure has not.

Australia maintained its Indo-Pacific engagement posture. Australian defence cooperation with Japan and the Philippines continued to deepen, fitting into a broader pattern of what analysts describe as the hardening of the first island chain as a zone of coordinated resistance to PLA expansion.

THEMATIC ANALYSIS

CYBERSECURITY

The cyber threat environment remained severe during the period under review, with both state-aligned actors and criminal networks active.

CISA issued an emergency directive on 19 June requiring federal agencies to patch CVE-2026-20253, an unauthenticated remote code execution vulnerability, within three days. The speed of the directive signals that active exploitation was assessed as either underway or imminent.

SecurityWeek reported on 18 June that a Conti gang associate, Oleksii Oleksiyovych Lytvynenko, admitted to working on the development of a loader for the criminal group -- a development that offers a window into the evolving Conti ecosystem, which has continued to operate in fragmented form following its 2022 public implosion.

OnyxC2, a new command-and-control malware variant, was flagged by researchers as targeting more than 200 applications and browser extensions, using encrypted payloads, DLL sideloading, and in-memory execution to evade detection.

The most structurally significant cyber trend of 2026 to date is not any single attack but the convergence of artificial intelligence with offensive operations. Device code attacks -- a technique that uses legitimate authentication flows to hijack user sessions -- have increased 37 times year-on-year, with 18 or more active attack kits now circulating. AI-assisted phishing campaigns are generating personalised, contextually plausible lures at industrial scale.

Earlier in 2026, the Stryker Corporation attack by Iranian-linked Handala -- which triggered simultaneous factor resets on more than 200,000 corporate devices across 79 countries -- demonstrated the capacity for geopolitically motivated actors to deliver genuine operational disruption through cyber means. The attack was framed by the perpetrators as retaliation for a US military strike in Iran.

Singapore reported in February that China-linked group UNC3886 breached all four of the country’s major telecommunications providers. That breach is now assessed as part of a sustained regional intelligence collection programme targeting Southeast Asian communications infrastructure.

MARITIME SECURITY

The Strait of Hormuz remains the dominant maritime security story globally. Approximately 20 percent of the world’s oil supply and 20 percent of global LNG trade moved through the strait in 2025. Since late February 2026, shipping traffic through the chokepoint has been reduced to near zero for commercial purposes. The US naval blockade of Iranian ports added a second layer of disruption.

The MOU’s staged reopening timeline -- 60 days for mine clearance, with commercial traffic increasing progressively -- does not mean conditions will return to normal quickly. The EIA projects that full restoration of pre-conflict oil production and trade flows will not occur until early 2027. Insurance premiums for vessels transiting the Gulf region remain prohibitively high for many operators. Mine clearance in a contested maritime environment where trust between the parties is limited is technically and politically complex.

In the Red Sea, the Houthi threat remains latent. A MARAD advisory from late March 2026 notes that despite a pause in commercial shipping attacks following the October 2025 Israel-Gaza ceasefire, the Houthis retain capability and continue to pose a threat to US-associated, Israeli-linked, and Western-associated vessels. Risk Intelligence assessments confirm that threat levels for these categories remain elevated.

The Red Sea’s structural security fragility is a function of the Houthi movement’s demonstrated ability to re-activate its maritime interdiction campaign at low cost whenever its political calculations change. A resumption of hostilities between Israel and Hezbollah, or any perceived breach of the US-Iran MOU, could trigger new Red Sea attacks within days.

Piracy in the Gulf of Guinea continues at lower intensity than its 2020-2021 peak, but criminal maritime activity along West Africa’s coast remains structurally tied to the same governance failures and resource conflicts that drive Sahel instability.

HUMAN TRAFFICKING AND MIGRANT SMUGGLING

The second International Forum of Prosecutors countering human trafficking and migrant smuggling, held on 12 June, highlighted the role of transnational prosecution networks in dismantling criminal organisations that exploit displacement corridors.

The Libya-to-Europe corridor remains one of the most active human trafficking routes globally. Dutch prosecutor Petra Hoekstra described the prosecution of a network that stretched from detention camps in Libya to victim families in the Netherlands -- a supply chain of human exploitation that is institutional in scale.

Brazil continues to see high rates of forced labour trafficking, predominantly affecting young men aged 18 to 29, often moved within the country to agricultural or extractive industry work sites under conditions of debt bondage.

Southeast Asian scam centre operations -- which use trafficked labour to conduct cyber fraud against victims globally -- continued to generate enforcement interest. These operations, concentrated in Myanmar, Cambodia, and Laos, represent a convergence of human trafficking, cybercrime, and transnational organised crime that has proven difficult to dismantle because of the complicity of local and regional governance actors.

The Trump administration’s Caribbean drug boat strike programme has created a legal and ethical controversy that complicates the enforcement environment for maritime trafficking interdiction. When lethal force is applied to vessels without adequate intelligence to distinguish drug cargo from human cargo, the policy risks eliminating the very victims it claims to be protecting.

INTERNATIONAL DRUG TRAFFICKING

The flow of synthetic narcotics -- particularly fentanyl precursors through maritime container shipping -- remains a primary transnational organised crime concern in North America. US-China bilateral drug intelligence working group meetings, held in Colorado Springs in February 2026, reflected a continuing if fraught attempt to coordinate on precursor control.

The disruption of Iranian governance during the 2026 war created conditions of reduced law enforcement capacity along Afghan heroin transit routes through Iran and into Central Asia and Turkey. This creates a potential window for increased narcotics flow through these corridors in the near term, though the effect will take time to manifest in downstream markets.

In West Africa, the narcotics dimension of terrorism funding -- particularly JNIM’s diversification of revenue streams -- reflects a convergence that security analysts have tracked since at least 2018. Criminal revenue sustains jihadist operational capacity when state revenue or Gulf funding contracts.

SANCTIONS AND TRADE

The Iran MOU included immediate sanctions waivers and the right of Iran to sell oil freely during the 60-day negotiation period. The longer-term sanctions architecture will be subject to final deal negotiations, but the immediate relief signals to markets that Iranian oil exports will begin to re-enter global supply chains.

US tariff authority under Section 122 expires on 24 July without legislative action. Trump’s tariffs on EU goods, combined with NATO burden-sharing tension, have created a transatlantic trade environment that the G7 summit in Evian partially addressed but did not resolve. The next six weeks will determine whether the US deploys alternative legal instruments to maintain its tariff schedule or whether the expiry triggers a de facto reduction in trade barriers.

China’s rare earth export restrictions, which have affected critical minerals supply chains across G7 economies, were assessed at the Evian summit as costing each affected economy an estimated $1.5 trillion. European and Japanese industrial planning for the medium term is now structurally dependent on resolving this constraint.

ELECTIONS AND DOMESTIC POLITICS

Ethiopia held general elections on 1 June under conditions of significant political tension and ongoing internal security challenges.

In France, the VivaTech conference of 17-20 June provided a backdrop for the Franco-German announcement on sovereign technology definitions, which carries significant implications for European industrial and data policy.

Mark Carney’s address at Trinity College Dublin on 14 June -- characterising the current moment as a “global rupture” -- was interpreted across European capitals as a signal that Canada’s foreign policy posture is shifting toward a more assertive articulation of Western liberal values in the face of US unpredictability.

STRATEGIC IMPLICATIONS

THE HORMUZ DEAL IS A BEGINNING, NOT AN ENDING

The US-Iran MOU is the most significant diplomatic development of 2026. But its strategic implications are defined more by what it does not resolve than by what it does.

Iran’s nuclear programme remains the central unresolved question. The IAEA cannot confirm the state of Iran’s enriched uranium stockpile following the 2025 strikes. If Iran retains sufficient material and technical capacity to build a weapon within weeks, the entire 60-day negotiation process begins from a position of fundamental information asymmetry favouring Tehran.

The MOU’s 60-day window is almost certainly insufficient to resolve the most contentious issues. History suggests these windows are extended, agreed frameworks collapse, or final deals contain ambiguities that allow both sides to claim victory while leaving core disputes unresolved. The Council on Foreign Relations noted the deal “creates a process” rather than a settlement. This is accurate.

For energy markets, the strategic implication is cautious optimism. Brent crude at $105 in June will fall as the strait reopens, but the EIA’s projection that prices will reach approximately $70 per barrel by the fourth quarter of 2026 is contingent on mine clearance proceeding, no further military incidents, and OPEC+ managing the production ramp-up effectively. Each of these conditions carries uncertainty.

CHINA IS MOVING IN THE SHADOW OF THE IRAN DEAL

The dominant narrative of the week was the US-Iran deal. That narrative created cover for China to escalate grey-zone pressure in the South China Sea without attracting proportionate international attention.

The sanctioning of the Philippine Defence Secretary is a significant escalation. The coordinated patrol of Taiwan’s Pratas Island by CCG and research vessels represents a methodical expansion of the normalisation strategy Beijing has applied in the South China Sea for more than a decade. Today’s normalisation becomes tomorrow’s baseline, and tomorrow’s baseline becomes next year’s contested territory.

The Trump-Xi summit of May generated ambiguity about US commitments to Taiwan. Beijing is exploiting that ambiguity deliberately and systematically. The 60-day window of the Iran deal negotiations will further absorb US diplomatic bandwidth. Expect Chinese maritime activity in the South China Sea to continue escalating during this period.

THE SAHEL IS APPROACHING A THRESHOLD

The African continent’s jihadist emergency is not being treated with the urgency it demands. CSIS’s characterisation of African terrorist groups as “unquestionably ascendant” -- fielding larger forces with better resources and increasing technological sophistication -- is a direct challenge to the assumption that terrorism is primarily a Middle Eastern or Central Asian phenomenon.

The US has withdrawn or reduced its military footprint in the Sahel. Russian Wagner Group successors have partially filled the vacuum, but their capacity and strategic coherence is limited. The convergence of jihadist networks, criminal trafficking organisations, and climate-driven displacement is creating conditions for cascading state failures. The risk is not that one Sahel country collapses -- Mali, Burkina Faso, and Niger have already crossed that threshold in practical terms -- but that the collapse expands southward into the Gulf of Guinea coastal states, which represent more substantial economies and populations.

THE UKRAINE WAR IS MOVING TOWARD AN UNCOMFORTABLE EQUILIBRIUM

Neither side has the capacity to achieve decisive military victory on the current trajectory. Russia cannot reconquer the territory it has lost. Ukraine cannot retake the occupied oblasts without a level of Western military support that has not been committed.

The polls showing 62 percent Russian support for negotiations and 61 percent Ukrainian support for territorial compromise represent an opportunity that has not yet been converted into a political framework. The US deadline of June has passed without resolution. The European insistence on coordination may preserve alliance coherence but narrows the diplomatic space for the kind of deal that Trump’s transactional approach might otherwise enable.

The risk is a long-term frozen conflict that drains European defence resources, perpetuates Ukrainian suffering, and enables Russian strategic patience. The tactical battlefield -- neither side gaining more than dozens of square miles in either direction over four-week periods -- reflects exactly this dynamic.

THE CYBER THREAT IS STRUCTURALLY OUTPACING DEFENCES

The 37-fold increase in device code attacks year-on-year, the proliferation of AI-assisted phishing, and the demonstrated capacity of state-aligned actors to deliver cross-border operational disruption through cyber means -- the Stryker attack being the clearest 2026 example -- indicate a threat environment that is intensifying faster than defensive capacity is expanding.

Critical infrastructure operators, healthcare systems, and telecommunications providers remain systematically under-defended relative to the sophistication of the threats they face. CISA’s three-day emergency patch directive reflects a regulatory environment that is increasingly reactive rather than proactive. The convergence of AI with offensive cyber tools is the most significant medium-term escalation risk in this domain.

WHAT TO WATCH NEXT

The following developments carry the highest analytical significance in the coming two to four weeks.

IRAN NUCLEAR TALKS: The 60-day negotiating window begins now. Watch for whether Iran accepts constraints on its enriched uranium or whether the nuclear question becomes the deal-breaker. Any IAEA access to Iranian facilities would be a significant positive indicator. Any Iranian resumption of enrichment to weapons-grade levels would be a critical negative indicator requiring immediate reassessment.

STRAIT OF HORMUZ REOPENING TIMELINE: Mine clearance operations in the strait will be the first practical test of Iranian commitment to the MOU. Watch for reports of vessels transiting without incident, and for the pace at which insurance underwriters begin offering commercially viable coverage for Gulf transit.

ISRAEL’S RESPONSE TO THE MOU: Netanyahu’s request for a direct meeting with Trump signals Israeli unhappiness with the deal. Watch for Israeli unilateral military action in Lebanon or against Iranian nuclear sites as the primary risk scenario that could unravel the MOU within the 60-day window.

US TARIFF CLIFF ON 24 JULY: The expiry of Section 122 authority will determine whether the global trade architecture of the past year is sustained, softened, or abruptly changed. Watch for congressional legislative action, White House executive orders, or informal diplomatic signals to allies in the coming three weeks.

CHINA IN THE SOUTH CHINA SEA: Expect continued CCG operations near Pratas Island and increased military signalling around Taiwan. The Philippines-Japan security cooperation announcement, combined with ASEAN Code of Conduct talks, will be the primary regional response mechanism. Watch for any Chinese action against Philippine resupply missions to BRP Sierra Madre at Ayungin Shoal.

SAHEL SECURITY ARCHITECTURE: The AU-ECOWAS joint engagement in Abuja is a critical institutional test. Watch for whether it produces coordinated counter-terrorism commitments or dissolves into procedural process, which would confirm the institutional gap that jihadist groups are already exploiting.

UKRAINE BATTLEFIELD AND DIPLOMATIC TRACK: Watch for any fresh US diplomatic engagement following the Iran deal’s signing. Trump’s attention to Ukraine will increase or decrease depending on whether the Iran process is perceived as a political success requiring consolidation or as a burden requiring delegation.

HEZBOLLAH DRONE WARFARE: Israel’s stated “unlimited budget” to counter fiber-optic FPV drones is a significant commitment. Watch for reports of Israeli tactical success or failure in countering this capability, as the outcome will shape the broader assessment of whether the MOU’s “including in Lebanon” formulation is viable.

SCENARIO OUTLOOK

Three scenarios define the medium-term strategic landscape through the end of Q3 2026.

SCENARIO ONE: MANAGED STABILISATION (Probability: 35 percent) The US-Iran MOU holds. Mine clearance proceeds. The Strait of Hormuz reopens to commercial traffic by mid-July. Oil prices fall toward $85 by September. The 60-day nuclear talks produce a framework agreement that defers the hardest questions. Israel remains frustrated but does not act unilaterally. Ukraine talks produce a tentative territorial proposal by autumn. US tariff authority is partially replaced by alternative legal instruments, softening but not eliminating the trade tension.

SCENARIO TWO: PARTIAL BREAKDOWN (Probability: 45 percent) The most likely scenario. The MOU holds on the Hormuz opening but nuclear talks stall at week four when Iran declines to commit to uranium limits. Israel conducts a limited strike on a Hezbollah weapons depot in Lebanon, prompting limited Iranian retaliation and raising the risk premium on the 60-day framework. Oil prices remain elevated. US tariff authority lapses on 24 July without clear replacement, creating a brief period of legal and market uncertainty. Ukraine remains frozen.

SCENARIO THREE: RENEWED ESCALATION (Probability: 20 percent) Israel conducts a significant unilateral strike against Iranian nuclear infrastructure within the 60-day window, arguing that the MOU does not constrain its right of self-defence. Iran responds by closing the Strait of Hormuz and suspending nuclear talks. The ceasefire collapses. US political pressure on Israel is insufficient to restore the framework in the near term. Oil prices spike above $120. European energy security enters emergency conditions. The scenario is unlikely but carries catastrophic downside risk.

CLOSING CONTEXT

The week of 14 to 20 June 2026 will be remembered as the week the world held its breath and exhaled, cautiously. The US-Iran MOU is real, its significance is real, and the relief in energy markets is real. But the architecture of the deal is thin, the unresolved questions are enormous, and the geopolitical environment in which the 60-day clock is now running is as unstable as any in recent memory.

China is not pausing. Sahel jihadism is not pausing. Ukrainian suffering is not pausing. Ransomware operators are not pausing. The drug and trafficking networks that exploit displacement corridors are not pausing. And the political will to address each of these challenges is fragmented across an alliance structure whose trust levels are, by the data, at historic lows.

The deal signed at Versailles is the beginning of a process. The process is uncertain. The world is watching.

DOWNLOAD FULL REPORT

SOURCES AND LINKS

The following sources were consulted in the preparation of this report. All links are listed here and do not appear elsewhere in the text.

Britannica - 2026 Iran War https://www.britannica.com/event/2026-Iran-war

UK House of Commons Library - US-Iran Ceasefire and Nuclear Talks 2026 https://commonslibrary.parliament.uk/research-briefings/cbp-10637/

PBS NewsHour - US and Iran reach initial deal to end war and reopen Strait of Hormuz https://www.pbs.org/newshour/amp/world/iran-and-u-s-reach-an-initial-deal-to-extend-the-ceasefire-and-open-the-strait-of-hormuz-but-challenges-remain

NBC News - Trump and Iran sign deal https://www.nbcnews.com/world/iran/strait-hormuz-reopen-us-lift-iran-sanctions-14-point-deal-seeking-end-rcna350513

Al Jazeera - US and Iran sign MOU https://www.aljazeera.com/news/2026/6/17/iran-confirms-that-mou-has-been-signed-electronically-by-both-sides

Newsweek - Trump’s 14-Point US-Iran Peace Deal https://www.newsweek.com/us-iran-14-point-deal-uranium-sanctions-hormuz-draft-12087032

CBC News - US and Iran sign deal including Strait of Hormuz plan https://www.cbc.ca/news/world/iran-us-war-memorandum-details-9.7238245

Council on Foreign Relations - The Iran Deal Reopens the Strait https://www.cfr.org/articles/trumps-iran-deal-reopens-the-strait-much-remains-to-be-done

NPR - US and Iran announce initial deal https://www.npr.org/2026/06/15/nx-s1-5858590/us-iran-deal-updates

ZeroFox - Monthly Geopolitical Report June 2026 https://www.zerofox.com/intelligence/monthly-geopolitical-report-june-2026/

Russia Matters - Russia-Ukraine War Report Card June 3 2026 https://www.russiamatters.org/news/russia-ukraine-war-report-card/russia-ukraine-war-report-card-june-3-2026

UK House of Commons Library - Developments in Ukraine Peace Talks https://commonslibrary.parliament.uk/research-briefings/cbp-10251/

France in the US - Outcomes of G7 Summit Evian https://us.diplomatie.gouv.fr/en/outcomes-evian-g7-summit

Atlantic Council - Seven Charts That Will Define France’s G7 Summit https://www.atlanticcouncil.org/dispatches/seven-charts-that-will-define-frances-g7-summit/

Euronews - Wars, Tariffs and AI: What to Expect from G7 in Evian https://www.euronews.com/my-europe/2026/06/14/wars-tariffs-and-ai-what-to-expect-from-the-g7-summit-in-evian

TechTimes - G7 Summit 2026 Iran Hormuz Deal Tariff Deadline https://www.techtimes.com/articles/318327/20260613/g7-summit-2026-iran-hormuz-deal-tariff-deadline-rare-earth-crisis-hit-evian.htm

AEI - China and Taiwan Update June 18 2026 https://www.aei.org/articles/china-taiwan-update-june-18-2026/

AEI - China and Taiwan Update June 12 2026 https://www.aei.org/articles/china-taiwan-update-june-12-2026/

AEI - China and Taiwan Update June 5 2026 https://www.aei.org/articles/china-taiwan-update-june-5-2026/

South China Morning Post - Quiet Escalation Around Taiwan’s Remote Outposts https://www.scmp.com/news/china/military/article/3357065/quiet-escalation-unfolding-around-taiwans-remote-outposts-beijing-sends-ships

Global Taiwan Institute - China’s Next Target in the South China Sea https://globaltaiwan.org/2026/05/chinas-next-target/

Defense News - Experts Warn Terrorism Threat Rising in Africa as US Pulls Back https://www.defensenews.com/news/pentagon-congress/2026/06/03/experts-warn-terrorism-threat-is-rising-in-africa-as-us-pulls-back/

African Security Analysis - West Africa Regional Security Architecture https://www.africansecurityanalysis.com/reports

ADF Magazine - Terrorism Takes Root https://adf-magazine.com/2026/05/terrorism-takes-root/

CFR - Violent Extremism in the Sahel https://www.cfr.org/global-conflict-tracker/conflict/violent-extremism-sahel

EIA - June 2026 Short-Term Energy Outlook https://www.eia.gov/pressroom/releases/press589.php

World Bank - Strait of Hormuz Disruption Sends Oil Prices Surging https://blogs.worldbank.org/en/opendata/strait-of-hormuz-disruption-sends-oil-prices-surging

IEA - Oil Market Report May 2026 https://www.iea.org/reports/oil-market-report-may-2026

IEA - The Middle East and Global Energy Markets https://www.iea.org/topics/the-middle-east-and-global-energy-markets

IEEFA - Impact of Middle East Crisis on Global Energy Markets https://ieefa.org/impact-middle-east-crisis-global-energy-markets

CSIS - Significant Cyber Incidents https://www.csis.org/programs/strategic-technologies-program/significant-cyber-incidents

SecurityWeek https://www.securityweek.com/

The Hacker News https://thehackernews.com/

MARAD - 2026-006 Red Sea Houthi Advisory https://www.maritime.dot.gov/msci/2026-006-red-sea-bab-el-mandeb-strait-gulf-aden-arabian-sea-and-somali-basin-houthi-attacks

Global Security Review - Red Sea Uncertainty 2026 https://globalsecurityreview.com/red-sea-uncertainty-a-2026-forecast-for-the-houthis-actions/

UNODC - Human Trafficking Latest News https://www.unodc.org/unodc/human-trafficking/latest-news.html

The Intercept - Trump Boat Strikes and Human Trafficking https://theintercept.com/2026/06/10/trump-boat-strikes-human-trafficking-victims/

EY - Geostrategic Analysis June 2026 https://www.ey.com/en_gl/insights/geostrategy/geostrategic-analysis

Lazard - Top Geopolitical Trends 2026 https://www.lazard.com/research-insights/top-geopolitical-trends-in-2026/

Wikipedia - 2026 Strait of Hormuz Crisis https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis

Wikipedia - 2026 Russia-Ukraine Truce (April) https://en.wikipedia.org/wiki/April_2026_Russo-Ukrainian_truce

| A guest post by

|